Page 336 - CA Final PARAM Digital Book.

P. 336

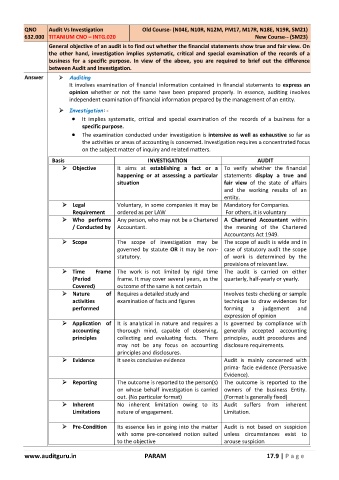

QNO Audit Vs Investigation Old Course- (N04E, N10R, N12M, PM17, M17R, N18E, N19R, SM21)

632.000 TITANIUM CNO – INTG.020 New Course-- (SM23)

General objective of an audit is to find out whether the financial statements show true and fair view. On

the other hand, investigation implies systematic, critical and special examination of the records of a

business for a specific purpose. In view of the above, you are required to brief out the difference

between Audit and Investigation.

Answer ➢ Auditing

It involves examination of financial information contained in financial statements to express an

opinion whether or not the same have been prepared properly. In essence, auditing involves

independent examination of financial information prepared by the management of an entity.

➢ Investigation: -

• It implies systematic, critical and special examination of the records of a business for a

specific purpose.

• The examination conducted under investigation is intensive as well as exhaustive so far as

the activities or areas of accounting is concerned. Investigation requires a concentrated focus

on the subject matter of inquiry and related matters.

Basis INVESTIGATION AUDIT

➢ Objective It aims at establishing a fact or a To verify whether the financial

happening or at assessing a particular statements display a true and

situation fair view of the state of affairs

and the working results of an

entity.

➢ Legal Voluntary, in some companies it may be Mandatory for Companies.

Requirement ordered as per LAW For others, it is voluntary

➢ Who performs Any person, who may not be a Chartered A Chartered Accountant within

/ Conducted by Accountant. the meaning of the Chartered

Accountants Act 1949.

➢ Scope The scope of investigation may be The scope of audit is wide and in

governed by statute OR it may be non- case of statutory audit the scope

statutory. of work is determined by the

provisions of relevant law.

➢ Time Frame The work is not limited by rigid time The audit is carried on either

(Period frame. It may cover several years, as the quarterly, half-yearly or yearly.

Covered) outcome of the same is not certain

➢ Nature of Requires a detailed study and Involves tests checking or sample

activities examination of facts and figures technique to draw evidences for

performed forming a judgement and

expression of opinion

➢ Application of It is analytical in nature and requires a Is governed by compliance with

accounting thorough mind, capable of observing, generally accepted accounting

principles collecting and evaluating facts. There principles, audit procedures and

may not be any focus on accounting disclosure requirements.

principles and disclosures.

➢ Evidence It seeks conclusive evidence Audit is mainly concerned with

prima- facie evidence (Persuasive

Evidence).

➢ Reporting The outcome is reported to the person(s) The outcome is reported to the

on whose behalf investigation is carried owners of the business Entity.

out. (No particular format) (Format is generally fixed)

➢ Inherent No inherent limitation owing to its Audit suffers from inherent

Limitations nature of engagement. Limitation.

➢ Pre-Condition Its essence lies in going into the matter Audit is not based on suspicion

with some pre-conceived notion suited unless circumstances exist to

to the objective arouse suspicion

www.auditguru.in PARAM 17.9 | P a g e