Page 11 - 30. COMPILER QB - IND AS 101

P. 11

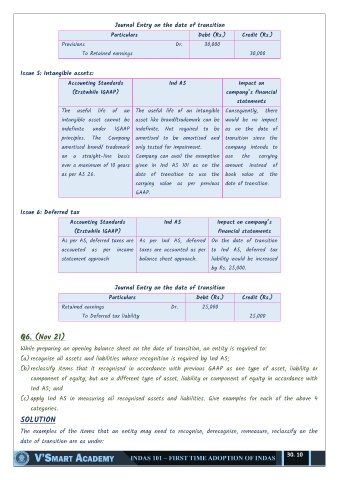

Journal Entry on the date of transition

Particulars Debt (Rs.) Credit (Rs.)

Provisions Dr. 30,000

To Retained earnings 30,000

Issue 5: Intangible assets:

Accounting Standards Ind AS Impact on

(Erstwhile IGAAP) company’s financial

statements

The useful life of an The useful life of an intangible Consequently, there

intangible asset cannot be asset like brand/trademark can be would be no impact

indefinite under IGAAP indefinite. Not required to be as on the date of

principles. The Company amortised to be amortised and transition since the

amortised brand/ trademark only tested for impairment. company intends to

on a straight-line basis Company can avail the exemption use the carrying

over a maximum of 10 years given in Ind AS 101 as on the amount instead of

as per AS 26. date of transition to use the book value at the

carrying value as per previous date of transition.

GAAP.

Issue 6: Deferred tax

Accounting Standards Ind AS Impact on company’s

(Erstwhile IGAAP) financial statements

As per AS, deferred taxes are As per Ind AS, deferred On the date of transition

accounted as per income taxes are accounted as per to Ind AS, deferred tax

statement approach balance sheet approach. liability would be increased

by Rs. 25,000.

Journal Entry on the date of transition

Particulars Debt (Rs.) Credit (Rs.)

Retained earnings Dr. 25,000

To Deferred tax liability 25,000

Q6. (Nov 21)

While preparing an opening balance sheet on the date of transition, an entity is required to:

(a) recognise all assets and liabilities whose recognition is required by Ind AS;

(b) reclassify items that it recognised in accordance with previous GAAP as one type of asset, liability or

component of equity, but are a different type of asset, liability or component of equity in accordance with

Ind AS; and

(c) apply Ind AS in measuring all recognised assets and liabilities. Give examples for each of the above 4

categories.

SOLUTION

The examples of the items that an entity may need to recognise, derecognise, remeasure, reclassify on the

date of transition are as under:

30. 10