Page 13 - 30. COMPILER QB - IND AS 101

P. 13

presented. The error should be corrected by restating the opening balances of relevant assets and/or liabilities

and relevant component of equity for the year 20X2-20X3. This will result in consequential restatement of

balances as at 1st April, 20X2 (i.e, opening balance sheet as at 1st April, 20X2).

Accordingly, on retrospective calculation of Share based options with respect to 80,000 options, Nuogen Ltd.

will create ‘Share based payment reserve (equity)’ by Rs. 16,00,000 and correspondingly adjust the same

though Retained earnings.

For 40,000 share based options to be vested on 31st March, 20X5:

Since share-based options have not been vested before transition date, no option as per Ind AS 101 is available

to Nuogen Ltd. The entity will apply Ind AS 102 retrospectively. However, Nuogen Ltd. did not account for the

same at the grant date. This will result in consequential restatement of balances as at 1st April, 20X2 (i.e,

opening balance sheet as at 1st April, 20X2). Adjustment is to be made by recognising the ‘ Share based

payment reserve (equity)’ and adjusting the retained earnings by Rs. 2,00,000.

Further, expenses for the year ended 31st March, 20X3 and share based payment reserve (equity) as at 31st

March, 20X3 were understated because of non-recognition of ‘employee benefits expense’ and related reserve.

To correct the above errors in the annual financial statements for the year ended 31st March, 20X4, the

entity should restate the comparative amounts (i.e., those for the year ended 31 st March, 20X3) in the

statement of profit and loss. In the given case, ‘Share based payment reserve (equity)’ would be credited by

Rs. 2,00,000 and ‘employee benefits expense’ would be debited by Rs. 2,00,000

For the year ending 31st March, 20X4, ‘Share based payment reserve (equity)’ would be credited by Rs.

2,00,000 and ‘employee benefits expense’ would be debited by Rs. 2,00,000.

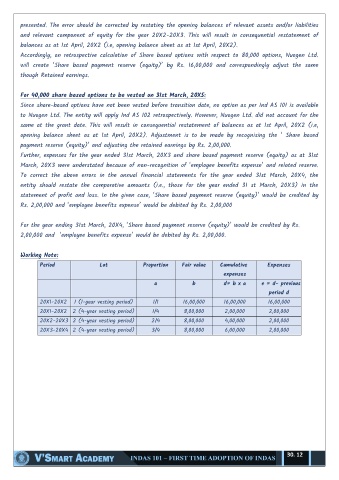

Working Note:

Period Lot Proportion Fair value Cumulative Expenses

expenses

a b d= b x a e = d- previous

period d

20X1-20X2 1 (1-year vesting period) 1/1 16,00,000 16,00,000 16,00,000

20X1-20X2 2 (4-year vesting period) 1/4 8,00,000 2,00,000 2,00,000

20X2-20X3 2 (4-year vesting period) 2/4 8,00,000 4,00,000 2,00,000

20X3-20X4 2 (4-year vesting period) 3/4 8,00,000 6,00,000 2,00,000

30. 12