Page 289 - CA Final PARAM Digital Book.

P. 289

QNO Gross NPA and Net NPA- Case Old Course – (N23R)

488.700 TITANIUM CNO -- Unique

PQS & Associates are one of the joint auditors of KNO Bank for the year 2022-23. While auditing KNO

Bank, they are analysing industry data relating to NPAs in select public sector banks as part of risk

assessment procedures: -

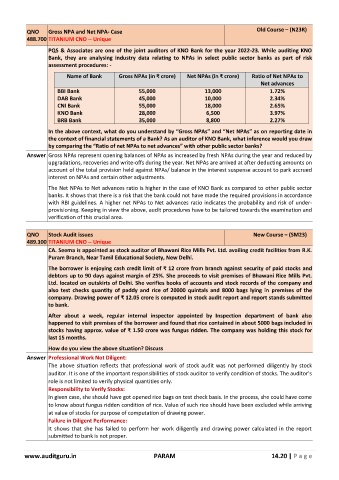

Name of Bank Gross NPAs (in ₹ crore) Net NPAs (in ₹ crore) Ratio of Net NPAs to

Net advances

BBI Bank 55,000 13,000 1.72%

DAB Bank 45,000 10,000 2.34%

CNI Bank 55,000 18,000 2.65%

KNO Bank 28,000 6,500 3.97%

BRB Bank 35,000 8,800 2.27%

In the above context, what do you understand by “Gross NPAs” and “Net NPAs” as on reporting date in

the context of financial statements of a Bank? As an auditor of KNO Bank, what inference would you draw

by comparing the “Ratio of net NPAs to net advances” with other public sector banks?

Answer Gross NPAs represent opening balances of NPAs as increased by fresh NPAs during the year and reduced by

upgradations, recoveries and write-offs during the year. Net NPAs are arrived at after deducting amounts on

account of the total provision held against NPAs/ balance in the interest suspense account to park accrued

interest on NPAs and certain other adjustments.

The Net NPAs to Net advances ratio is higher in the case of KNO Bank as compared to other public sector

banks. It shows that there is a risk that the bank could not have made the required provisions in accordance

with RBI guidelines. A higher net NPAs to Net advances ratio indicates the probability and risk of under-

provisioning. Keeping in view the above, audit procedures have to be tailored towards the examination and

verification of this crucial area.

QNO Stock Audit issues New Course – (SM23)

489.100 TITANIUM CNO -- Unique

CA. Seema is appointed as stock auditor of Bhawani Rice Mills Pvt. Ltd. availing credit facilities from R.K.

Puram Branch, Near Tamil Educational Society, New Delhi.

The borrower is enjoying cash credit limit of ₹ 12 crore from branch against security of paid stocks and

debtors up to 90 days against margin of 25%. She proceeds to visit premises of Bhawani Rice Mills Pvt.

Ltd. located on outskirts of Delhi. She verifies books of accounts and stock records of the company and

also test checks quantity of paddy and rice of 20000 quintals and 8000 bags lying in premises of the

company. Drawing power of ₹ 12.05 crore is computed in stock audit report and report stands submitted

to bank.

After about a week, regular internal inspector appointed by Inspection department of bank also

happened to visit premises of the borrower and found that rice contained in about 5000 bags included in

stocks having approx. value of ₹ 1.50 crore was fungus ridden. The company was holding this stock for

last 15 months.

How do you view the above situation? Discuss

Answer Professional Work Not Diligent:

The above situation reflects that professional work of stock audit was not performed diligently by stock

auditor. It is one of the important responsibilities of stock auditor to verify condition of stocks. The auditor’s

role is not limited to verify physical quantities only.

Responsibility to Verify Stocks:

In given case, she should have got opened rice bags on test check basis. In the process, she could have come

to know about fungus ridden condition of rice. Value of such rice should have been excluded while arriving

at value of stocks for purpose of computation of drawing power.

Failure in Diligent Performance:

It shows that she has failed to perform her work diligently and drawing power calculated in the report

submitted to bank is not proper.

www.auditguru.in PARAM 14.20 | P a g e